The intraday electricity market is the operational core of modern power trading, where energy positions are continuously adjusted in response to real-world conditions. In this continuous trading environment, generators, suppliers, traders, and large consumers buy and sell electricity on the same day as physical delivery, right up to the moment power flows through the grid. Operating 24 hours a day, 365 days a year, across major European exchanges such as EPEX SPOT and Nord Pool, it is the market where planning meets execution.

While the day-ahead market (DAM) sets the baseline plan for the following day, the intraday market (IDM) exists to manage everything that deviates from that plan. In a system increasingly dominated by variable renewable energy sources like wind and solar, those deviations are not exceptions, they are constant. Forecast errors, unexpected outages, and real-time consumption changes all create imbalances that must be resolved before delivery, and the intraday market is where that correction happens.

Our guide is divided into two parts. In this first part, we cover the market structure, trading products, and fundamental mechanics that define short-term power trading in Europe in 2026.

In the second part, we explain how to trade power intraday, key trading strategies, and algorithms. To learn more, check: Intraday Power Trading 2: How to Trade & Strategies & Algorithms

What is Intraday Power Trading?

Intraday power trading is where energy plans meet physical reality. The day-ahead market sets the position. The intraday market is where that position gets tested, refined, and corrected as real-world conditions diverge from the forecast. For any participant managing generation assets, consumption portfolios, or trading books, it is the most operationally demanding part of the trading cycle and the one with the least margin for error.

Why the Intraday Market Exists?

Electricity cannot be stored at scale. Generation and consumption must match at every moment to maintain grid frequency stability, which is the measure of whether supply and demand are in balance across the entire network. In Europe, the grid operates at a constant frequency of 50 Hz. Even a small deviation from this frequency caused by a mismatch between generation and consumption can damage equipment and trigger blackouts.

When participants fall out of balance, the Transmission System Operator (TSO), the body responsible for keeping the grid stable, intervenes with balancing reserves at costs passed directly to the participants responsible for the imbalance.

The intraday market gives participants the mechanism to correct their own position before that happens. Wind and solar output changes continuously and is never forecast perfectly 24 hours in advance. The closer to delivery a participant can trade, the more accurate their forecast and the smaller their residual imbalance.

Who Uses Intraday Power Trading?

Anyone who puts electricity into the grid or takes it out needs the intraday market to stay safe and profitable.

- Renewable energy producers use the intraday market to update positions as short-range weather forecasts improve closer to delivery. A wind farm that overcommitted in the day-ahead market sells its surplus. One that underperformed buys back its shortfall.

- Conventional power plant operators use it to adjust output around unplanned technical constraints or to respond to price movements that make increasing or reducing generation commercially worthwhile.

- Large industrial consumers use it to offload purchased energy they can no longer use. When an unplanned production outage reduces consumption below a contracted position, the intraday market is where that surplus gets sold.

- Energy traders use it to capture intraday price spreads, buying during periods of excess renewable generation when prices are depressed and selling when demand-driven price spikes occur.

What is a Balancing Responsible Party (BRP)?

A Balancing Responsible Party (BRP) is the legal entity financially responsible for ensuring that its scheduled energy production or consumption matches what actually happens. Every participant that puts electricity into the grid or takes it out belongs to a BRP. If a BRP’s actual behaviour deviates from its schedule, it creates an imbalance. The TSO charges BRP for the cost of correcting the imbalance using balancing reserves. The intraday market is the primary tool BRPs use to avoid those charges by correcting their own position before gate closure.

| Term | Definition |

|---|---|

| Intraday Market | The market where electricity is traded on the same day as physical delivery |

| Day-Ahead Market | The market where electricity is traded the day before delivery at a uniform clearing price |

| Pay-As-Bid | A pricing model where every trade settles at the exact price agreed between buyer and seller |

| Gate Closure | The deadline after which no more trades can be made for a specific delivery slot |

| Lead Time | The time between Gate Closure and the start of physical delivery |

| TSO | Transmission System Operator, the body responsible for grid stability |

| Market Clearing Price | The single price at which maximum auction volume can be matched |

| Central Order Book | The live digital list of all active buy and sell orders in the market |

| Balancing Responsible Party (BRP) | The legal entity is financially responsible for matching the scheduled and actual energy flow |

| OTC Trading | Private bilateral contracts are negotiated directly between two parties outside a regulated exchange |

| Short-Term Wholesale Market | A trading venue where professional participants buy and sell electricity close to delivery time |

| Grid Frequency | The measure of balance between generation and consumption across the network is maintained at 50 Hz in Europe |

Intraday Trading Products – Market Coupling (SIDC)

The day-ahead market establishes the system’s reference plan, while the intraday market exists to manage real-time deviations from that plan. However, in systems with a high share of renewable energy generation, hourly products are often too coarse to effectively capture these deviations.

This is where the Single Intraday Coupling (SIDC) comes into play. SIDC is not a product, but a shared trading infrastructure that connects local electricity markets across Europe and continuously optimises cross-border capacity in real time. Through this mechanism, 15-minute, 30-minute, and hourly products are no longer confined to local markets; they become tradable units of flexibility that can flow across the continent.

By enabling this continuous cross-border liquidity, SIDC transforms time-based products into a system-wide balancing tool. It effectively matches the speed and flexibility of your energy assets with the depth of the entire European market, allowing participants to manage positions with far greater precision.

Rather than imposing a single standard, the vast liquidity pool created by SIDC provides market participants with multiple time resolutions to choose from, depending on the responsiveness and operational characteristics of their assets.

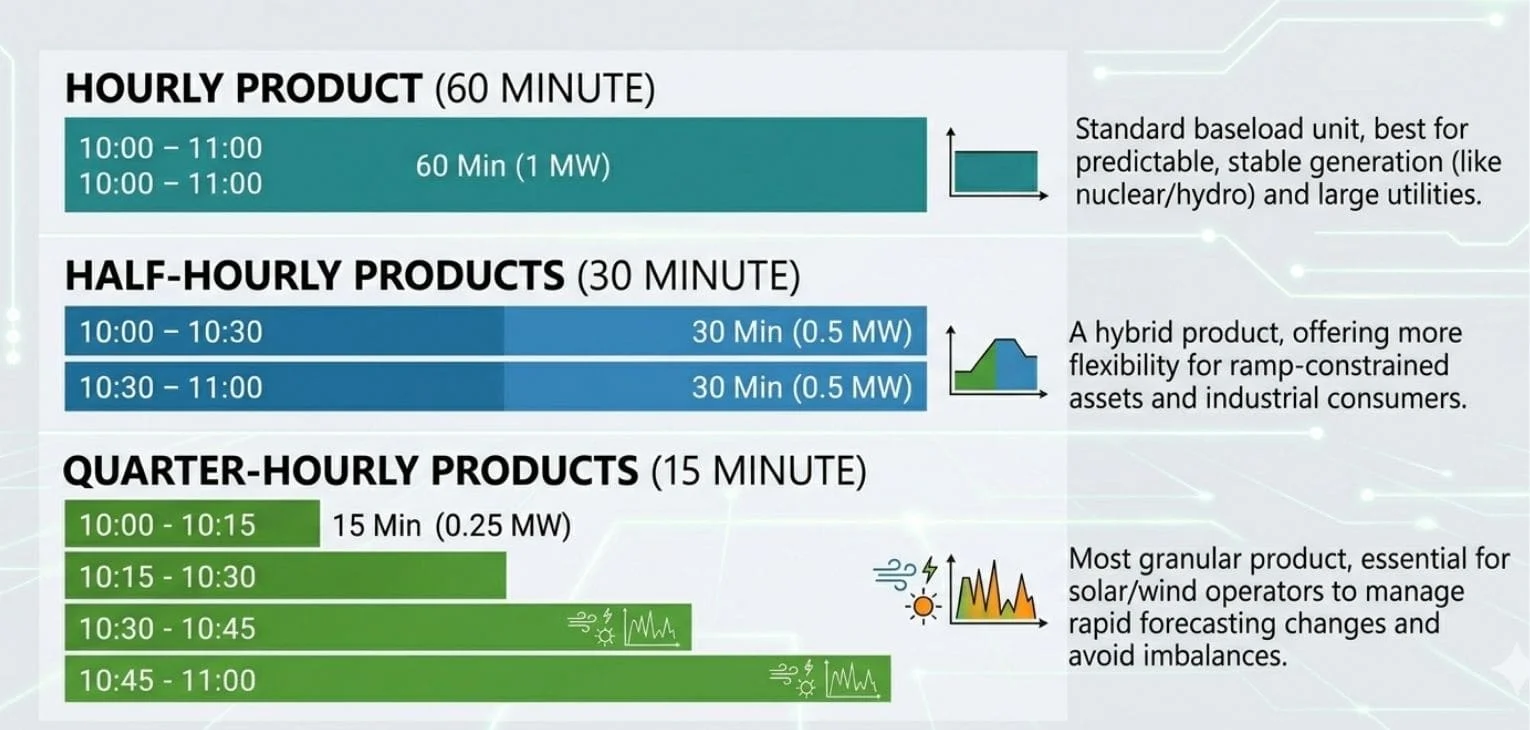

The 15-Minute Product

In 2026, the 15-minute product is the core of European intraday power trading. When a solar park comes online at dawn, its output does not climb in neat hourly steps. It ramps gradually, then quickly, then gradually again as the sun tracks across the sky. An hourly product cannot capture that curve. A 15-minute product can let traders sell in a staircase pattern that reflects what their asset is actually doing in real time.

The 15-minute product serves two distinct purposes:

- Ramping management: It allows renewable producers to match their contracted position to the actual output curve of their asset, interval by interval, rather than committing to a flat hourly volume that rarely reflects reality.

- Imbalance avoidance: TSOs settle imbalances on a 15-minute basis. If a participant is out of balance for even one quarter-hour window, they pay for it. The 15-minute product is the only instrument that fully resolves this exposure.

The Half-Hourly Product

The 30-minute product serves as a practical middle ground between hourly planning and quarter-hourly execution. It is particularly relevant in three situations:

- Ramp-constrained assets: For power plants that need moderate ramp time to reach full capacity, half-hourly blocks allow operators to step up production more accurately than a 60-minute block permits.

- Cross-border synchronisation: At intersections where national grids with different market structures meet, 30-minute blocks are frequently used to reconcile supply and demand across borders where hourly and quarter-hourly conventions need to be bridged.

- Industrial consumers: Many large industrial facilities operate production cycles that align naturally with 30-minute intervals, making this product a practical hedging tool for managing energy costs against actual machine usage.

The Hourly Product

Despite the shift toward finer granularity, hourly products remain the primary reference point for the European wholesale market. They serve three core functions:

- Baseload efficiency: Large assets, including nuclear plants and major hydro facilities, use hourly blocks to sell high volumes without needing to adjust production every few minutes. The hourly block is the most stable and logistically efficient unit for assets that operate at consistent output levels.

- Price benchmarking: Most long-term contracts and day-ahead auctions are priced in hourly intervals, making the 60-minute block the benchmark against which all shorter-duration products are valued across the market.

- Cross-border flows: Much of the transmission capacity between European countries is still managed in hourly windows. For moving large volumes across the continent, the hourly product remains the most efficient instrument available.

Block Orders

Some assets simply cannot operate in 15-minute slices. A gas turbine needs a sustained run to justify its startup costs. A large thermal unit has minimum stable generation periods built into its mechanical design. Block orders exist to respect these physical realities.

- All-or-nothing execution: A four-hour block executes only if the entire four hours can be filled. If the market can absorb three hours but not the fourth, the whole order is rejected. No partial fills, no fragmented schedules that are physically impossible to honour.

- User-defined blocks: By 2026, exchanges support custom block windows, such as 06:15 to 09:45, letting operators match the exact startup and shutdown profile of a specific plant rather than forcing it into standardised time slots.

Linked Basket Orders & Exclusive Groups

For algorithmic traders and battery operators running complex multi-asset strategies, individual blocks are often insufficient. Two advanced order types address this:

- Linked basket orders: These introduce parent-child logic: buy 10 MW of solar production in the morning, but only if the corresponding battery discharge in the evening can also be sold. If one leg of the basket cannot be filled, the other automatically cancels. The trade only exists as a whole or not at all.

- Exclusive groups: A trader submits multiple versions of the same trade at different prices or volumes. The exchange selects the best executable option and automatically cancels the others, preventing the trader from accumulating duplicate positions across multiple scenarios.

| Product | Duration | Primary User | Core Purpose | Execution Logic |

|---|---|---|---|---|

| 15-Minute | 0.25 hours | Solar and wind operators | Ramping management and imbalance avoidance | Executes independently per quarter-hour slot |

| Half-Hourly | 0.5 hours | Ramp-constrained plants, industrial consumers, cross-border corridors | Bridging hourly planning and quarter-hourly execution | Executes independently per half-hour slot |

| Hourly | 1 hour | Nuclear, hydro, and large utilities | Baseload revenue and price benchmarking | Executes independently per hour slot |

| Block Order | 2 to 24 hours | Gas turbines and thermal plants | Minimum run time protection and startup cost recovery | All-or-nothing across the entire linked window |

| User-Defined Block | Custom window | Any asset with specific ramp profiles | Matching exact startup and shutdown schedules | All-or-nothing across the custom time window |

| Linked Basket | Variable | Batteries and algorithmic traders | Conditional multi-asset optimisation | All legs execute together or none execute at all |

| Exclusive Group | Variable | Algorithmic traders | Scenario hedging and preventing duplicate positions | Best executable option wins, all others auto-cancel |

Intraday vs. Day-Ahead Market: Key Differences

The day-ahead market and the intraday market serve two distinct purposes in the electricity trading cycle. The day-ahead market is a once-daily auction where participants commit to energy volumes for the following day at a single uniform clearing price, with gate closure at noon CET. The intraday market opens immediately after and runs continuously until minutes before physical delivery, allowing participants to correct their positions using real-time data.

The core difference is timing and pricing: Day-ahead uses uniform pricing set 12 to 36 hours before delivery, while the intraday market uses pay-as-bid pricing with lead times as short as five minutes.

The Structure of Short-Term Markets

Transparency across the European intraday electricity trading market is maintained through dedicated timelines and standardised operating platforms.

- Timelines and Gate Closure: Market efficiency relies on strict schedules. Day-ahead auctions are usually structured into hourly slots, though many regions have moved toward 30-minute or 15-minute granularity. Gate closure rules are the deadlines that dictate exactly when an offer must be submitted for a given delivery slot.

- The Role of Market Operators: Large operators ensure transparency across regional borders. EPEX SPOT services 13 European regions, while Nord Pool operates across 16 countries. These entities provide the digital infrastructure and data portals that allow participants to trade with confidence across regional borders.

Price Reference and Settlement Differences

Each market offers a different balance of risk and volume.

- Day-Ahead (The Plan): Better suited for high-volume, planned purchases. It uses a Single Uniform Price Auction, also called pay-as-clear, where every participant receives the same clearing price for a specific hour, regardless of their original bid.

- Intraday (The Reality): Offers the flexibility needed to react to real-time changes. It typically uses continuous trading with a pay-as-bid structure, where every trade settles at the exact price agreed at that moment. Market coupling integrates these national markets, allowing liquidity to flow where it is most needed across borders.

Managing Forecast Errors and Imbalance Exposure

The intraday market is the primary tool for correcting position imbalances. If a wind farm produces less than expected, the trader must buy back that shortfall before the market closes.

- Imbalance Settlement: If a participant still has a mismatch after the intraday gate closes, they are passed to the Balancing Mechanism. At this stage, the System Operator steps in to stabilise the grid, and the participant is charged imbalance fees that are often significantly more expensive than prevailing market prices.

- AI-Powered Forecasting: To stay ahead of position imbalances, traders increasingly integrate AI tools that analyse parameters such as temperature, wind speed, and solar irradiance. Probabilistic forecasting quantifies renewable energy output uncertainty, allowing traders to adjust their market positions before prices shift against them.

Trading Strategies for Volatile Conditions

- Intraday Spreads: Traders exploit price differences between two different time slots within the same trading day, entering positions ahead of anticipated price spikes and exiting once those spikes materialise.

- Risk Hedging: Spreading exposure across a diverse portfolio management, such as combining wind and solar assets, allows producers to offset underperformance in one asset with gains in another. Since weather conditions that suppress wind output often support solar generation and vice versa, portfolio diversification provides a natural partial hedge against renewable volatility.

- Algorithmic Trading: Speed is essential in the intraday market. Algorithms analyse large volumes of historical and real-time data, including weather signals and order book movements, in fractions of a second. This enables automated dispatch, where physical energy flows are adjusted automatically in response to market signals without manual intervention.

- Cross-Border Arbitrage: Traders buy energy in a lower-priced region and sell it simultaneously in a higher-priced area, capturing the price differential as profit. However, they must account for congestion rent, which is the fee charged by Transmission System Operators when demand for cross-border transmission capacity exceeds what is physically available on a given interconnector.

Success in short-term trading depends on precision, forecasting accuracy, and the ability to execute within minutes.

| Feature | Day-Ahead Market (DAM) | Intraday Market (IDM) |

|---|---|---|

| Primary Purpose | Establishing the “base” energy plan for the next day. | Adjusting for real-time deviations and unforeseen changes. |

| Trading Timeline | Once a day (usually by 12:00 CET for the next day). | Continuous (24/7) up until minutes before delivery. |

| Pricing Model | Market Clearing Price: All participants pay/receive the same uniform price. | Pay-as-Bid: Every transaction is settled at the specific price bid. |

| Granularity | Usually, hourly intervals (60 minutes). | Highly granular: hourly, half-hourly, and quarter-hourly (15 min). |

| Market Volatility | Moderate; based on broad forecasts and historical trends. | High; reacts instantly to sudden weather shifts or plant outages. |

| Lead Time | 12 to 36 hours before physical delivery. | Very short; ranges from 5 to 60 minutes before delivery. |

| Trading Method | Discrete blind auctions (one-time event). | Continuous trading (ongoing order book) and specific auctions. |

Conclusion: From Structure to Strategy

The intraday market is where electricity trading transitions from planning to real-time execution. As this first part has shown, its structure is defined by continuous trading, increasing time granularity, and a wide range of products designed to match the physical realities of different energy assets.

Understanding these fundamentals is essential, but it is only the starting point. The real competitive advantage in intraday trading comes from how participants use this structure: how they manage risk, respond to volatility, and execute decisions under time pressure.

Intraday trading performance is no longer determined by access to the market, but by how effectively you can act within it. If you are managing renewable assets, flexible capacity, or an active trading book, the difference between reacting late and executing in real time directly impacts your bottom line. smartPulse is designed to close that gap by combining algorithmic execution, data screens, and portfolio optimisation into a single platform built for modern power markets. Book a demo today to see how smartPulse can help you trade faster, reduce imbalance costs, and unlock new revenue opportunities in the intraday market.

In the second part of this guide, Intraday Power Trading 2: How to Trade & Strategies & Algorithms, we move beyond market structure into execution. We will explore why participants rely on intraday trading, the strategies they use to generate value, the challenges they face in a high-speed data-driven environment, and how algorithmic and autonomous systems are redefining performance in modern power markets.